Silver prices | Here's What the New <b>Silver Price</b> Fix Means for Prices |

- Here's What the New <b>Silver Price</b> Fix Means for Prices

- New <b>Silver Price</b> Fix Procedure :: The Market Oracle :: Financial <b>...</b>

- New 'LBMA <b>Silver Price</b>' Farce - Still Shockingly Non Transparent <b>...</b>

| Here's What the New <b>Silver Price</b> Fix Means for Prices Posted: 14 Aug 2014 01:29 PM PDT

And market observers are hoping that this new procedure for setting the silver price global benchmark will bring some much needed transparency to the process. Silver pricing could definitely stand to gain from more transparency, following a century-old mechanism that involved three banks negotiating prices in secret. The three member banks were facing lawsuits after accusations arose that they were manipulating prices, so it's no wonder that some are expecting a free market transition. "It certainly isn't a free market in that case," said Money Morning Resource Specialist Peter Krauth. "Without proper price discovery you don't have a healthy market." Here's how the new procedure will operate... The New Silver Pricing MechanismAt noon in London, an electronic auction will take place on a trading platform provided by CME Group Inc. Members will begin a bidding process at a price based off quoted rates for silver across the market. Members will process buy and sell volumes at the initial seed price for 30 seconds. If after that auction buy and sell volumes are in tolerance - that is, if they are within 300,000 ounces of each other - a new price will be set. If not, the auction will restart at a new price determined by an electronic algorithm. Auctions will continue to reset until the buy and sell orders are properly balanced at the prevailing price. The initial participants in the new silver fix are HSBC Bank (NYSE ADR: HSBC), Mitsui & Co. Precious Metals Inc., and ScotiaMocatta (a division of the Bank of Nova Scotia [NYSE: BNS]), but that is expected to grow in the coming weeks. Rhona O'Connell, head of metals at Thomson Reuters GFMS, told Money Morning in an email that the initial members are largely from the banking sector, but there are hopes that "that may expand into industry as time goes on." Thomson Reuters will handle governance and administration duties in the new pricing procedure. The Need for Transparency in Pricing SilverThe main concern about any price discovery mechanism for silver is transparency. "Everybody these days is worried that if something isn't totally transparent that there's going to be litigation at some stage if somebody's not happy with it," Steve Garwood, a trader at Baird & Co., told Bloomberg. The former silver fix involved a small coterie of banks, where the head of a fixing committee would, by his own individual decree, determine the price at which auctions would take place. It was often criticized for the secrecy and even drew litigation under the suspicion that prices were being manipulated. O'Connell said this new pricing model would deliver more transparency by giving market players the ability to monitor the buy and sell volumes offered in determining the price. As well as this, benchmark prices will be algorithmically calculated and independently determined, unlike the prior mechanism, in which it was settled on by an individual. But there's already reason to think the new process will have the same problems... The initial participants include three of the 11 market-making members of the London Bullion Market Association, and the other eight could join as the new fix matures. With similar names reentering the new silver pricing game, Money Morning's Krauth is slightly discouraged, believing that at least initially, the new fix won't allow for proper price discovery. "It's the same gang that a lot of observers did feel are not necessarily doing this in the most transparent and free-market-price-discovery-oriented kind of way," Krauth said. With the last silver pricing mechanism at the whim of a small collection of banks, there's reason to believe that if manipulation was occurring, it was only working to keep silver prices artificially low. The large number of short positions taken out by banks like JPM would suggest that the big banks stand to gain when silver falls. Even with that concern, these efforts in the new silver fix to be more transparent "might be a relatively small step toward a true market-determined price," Krauth said, and not a price artificially kept low to satiate institutional shorts. The demand fundamentals for silver are strong enough to drive up prices once it can un-wedge itself from the speculator's downward pricing pressure. "Despite persistently low silver prices, demand for physical silver witnessed an all-time high in 2013," Krauth said. "All the fundamental drivers for much higher silver prices are still intact, so now is a great time to position yourself for higher silver." Silver demand was at 1.1 billion ounces in 2013, according to the Silver Institute, which was a 13.3% increase from the year before. More from Peter Krauth: The London Silver Fix is officially gone after 117 years, unencumbering the white metal from the artificially low price fixes set by a small coterie of banks. With demand for physical silver hitting all-time highs, and market forces overtaking manipulation, now is the time to jump in on the coming silver bull market... Related Articles:

|

| New <b>Silver Price</b> Fix Procedure :: The Market Oracle :: Financial <b>...</b> Posted: 18 Aug 2014 08:15 AM PDT

By: Alasdair_Macleod

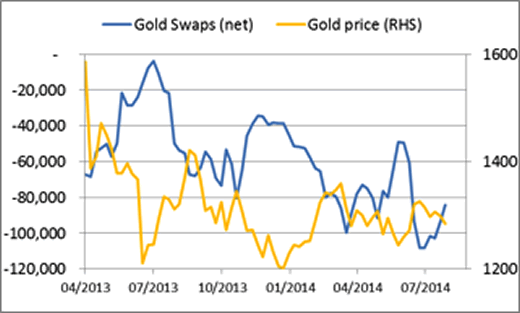

However, the underlying position is more positive than this limited move suggests, with the Swap category on Comex appearing to be in some difficulty. Swaps are mostly non-market making bullion banks. Their net short position on 5th August was 84,108 contracts, about 30,000 higher than their long term average, and while this may have reduced a little since then there is insufficient liquidity on Comex for them to close this collective net short without driving prices sharply higher. The chart below, which is from the dramatic knock-down in April 2013, shows net swaps are locked into a declining trend while the gold price stubbornly refuses to go any lower.

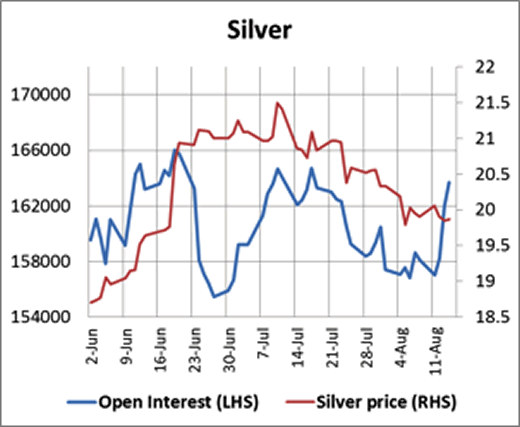

Obviously, Swaps trade most profitably on the bear tack in a falling market. This is visually represented in the chart by the blue line rising when the yellow line falls, and vice-versa. This clearly worked well until April this year when the gold price failed to respond to changes in the Swaps' net shorts. The result is Swaps are now net short to an uncomfortable degree with a price that is no longer falling. They have a similar problem in silver and the technical situation is potentially very strong as can be seen in the Open Interest chart below.

Open interest is rallying strongly while the price remains held under $20. This indicates someone or some parties are sitting on the price refusing to let it go higher The next break above $20 could see the price go substantially better. With the new London fix from today, it looks like Canute's attempt to stop an incoming tide of buyers. The new silver fix This is a welcome advance on the old silver fix, where bullion banks negotiate the price in secret. This should be positive in the longer-term, because market transparency tends to lead to wider institutional and public participation. We are a long way from a fully transparent market, but at least the veil of dealing secrecy is being lifted a little. Imagine you are running a hedge fund. You don't deal in gold or silver because the physical market is too opaque. Now we have a visible auction process in silver, which you can watch on-line. You can monitor it for a week or two to get better a feel for how much money is required to move the price. It's not just you, everyone else is also getting interested. Now you can assess your dealing risk far better and will be prepared to deal. And you look forward to the gold market becoming more transparent as well. To summarise, I believe we are seeing a very important change in bullion markets to the disadvantage of dealers who hide behind OTC opacity. Next week Alasdair Macleod Head of research, GoldMoney Alasdair.Macleod@GoldMoney.com Alasdair Macleod runs FinanceAndEconomics.org, a website dedicated to sound money and demystifying finance and economics. Alasdair has a background as a stockbroker, banker and economist. He is also a contributor to GoldMoney - The best way to buy gold online. © 2014 Copyright Alasdair Macleod - All Rights Reserved © 2005-2014 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication. |

| New 'LBMA <b>Silver Price</b>' Farce - Still Shockingly Non Transparent <b>...</b> Posted: 15 Aug 2014 05:33 AM PDT New 'LBMA Silver Price' Farce - Still Shockingly Non Transparent

(Credit: courtesy NM Rothschild) It's not entirely clear how the LBMA could know to step in at such notice on 14th May and begin an uncontested consultation process less than a few hours after an entirely separate organisation, the London Silver Market Fixing Company Ltd, announced that they were bowing out of the process. Perhaps the two organisations are not as distinct as they maintain to be. Throughout the new silver pricing "consultation" between mid-May and mid-August, the LBMA have maintained that they have been striving for transparency. But the process has been anything but transparent. During the last few days it has become apparent that the entire formulation and implementation of the new silver pricing process appears to have been rushed through, with market participants now fearful that a) they won't understand the new system since it's not user friendly, b) there is no clear information about the number and type of market participants that will be contributing to the price setting process, and c) it may not be able to provide a silver price benchmark for the myriad users who are depending on a silver price benchmark in order to price and hedge their silver products and act as a reference point for their contracts that previously used the existing London Silver Fixing price. Indeed, the LBMA have just updated their website regarding the newly selected administrators and governors of the silver price process, CME/Thomson Reuters, stating that "the process has been undertaken quickly and efficiently but the tight schedule and the time of the year has imposed time constraints on some potential participants seeking internal signoff on the necessary credit, legal, compliance and IT requirements. This means that not all those who have participated in the live trails will be accredited in time to participate on 15th August." This in itself is ludicrous. Why, given the time of year and the tight schedule, have the LBMA tried to railroad these changes through right now? There has been no public explanation as to why they have continued to try to push through this new process, especially in the last two weeks. This morning (August 15th) for the first time, the LBMA published the names of accredited participants in the new process. It is highly irregular that they have left the publication of the participants list until a few hours before the very first ever new silver price setting process. The LBMA states hopefully that they expect this participant list to grow over the coming weeks. But the questions remains, why were the LBMA exclusively involved in this whole process in the first place from the 14th May, and why are they now rushing through a system that the market appears to have doubts about, using a consultation process that was far from transparent? During the past week, silver market participants have been more than scathing about what they see as ill-preparedness by the LBMA and the winning bidder CME/Thomson Reuters. For example, last Tuesday 12th August, Ross Norman, a veteran precious metals trader in the London markets and a colleague of many other experienced precious metals traders said that "it remains a mystery who will be taking the fix orders – with a deafening silence from market participants." Norman also highlighted the totally bizarre change in the standard unit of a silver order in the new system, which has gone from US dollars per ounce, to a unit of 'lakh' which is 100,000 ounces. Ross, who began his career working for Sir Clive Sinclair of Sinclair Research in Cambridge, even likened the user interface of the new CME/Thomson Reuters silver trading platform to something from a command prompt MS-Dos user interface from the 1970s. He also pointed out, what to us looks like a conflict of interest for Reuters, that to follow the new silver setting process in real time, one needs to purchase a subscription to the Reuters Eikon (or Elektron) platform, and given that Thomson Reuters is responsible for administration and governance of the new price setting process, they will also benefit from users signing up to these platforms in order to follow the silver auctions. The new auction platform was not favourably received by various London based precious metals traders, as relayed by Ross Norman, but the language used was quite colourful so we will leave it to readers to search for these references. On Wednesday last 13th August, Courtney Lynn, Treasurer at Coeur Mining, was interviewed by Kitco News on the new silver price process and said the following in relation to the market's preparedness for the switchover; "We expected challenges in getting there, there's a lot of legal documentation, IT challenges that need to be worked out, and I know that all the banks are working full steam ahead to get there by Friday. Lynn explained that Coeur "use the silver fix in three different ways. We sell our metal on the fix, we hedge our metal against the fix, and we also use the benchmark in our royalty agreements for calculating royalty payments." Courtney Lynn went on to say that "A new process was needed, really to mitigate a lot of risk to the banks, and limit the regulatory, legal and reputational risk that they face. It's similar to LIBOR where you had a small group of banks setting a benchmark for a large industry….. It was somewhat surprising, the timing I guess, and the abrupt transition, but it needed to happen." "In this sort of environment and consultation process, we've tried to talk through what's important to us and communicate that to the industry and specifically the LBMA, because the LBMA represents largely banks and the banks have a big voice to begin with…we make sure…. that we had a seat at the table and made sure than our interests were met as well." Finally, Ross Norman stated succinctly on the new change, that "one is left to ponder whether this has done anything to address the requirement for efficiency and transparency". This is exactly our point in the discussion which follows. Below, we illustrate using multiple examples, exactly why this LBMA silver price consultation process was far from transparent, even as the LBMA continues to maintain the fiction that the process has been transparent. Part of the LBMA consultation consisted of an online survey which was launched on 16th May, two days after the LBMA became involved, the survey closing date of 30th May. The LBMA online survey consisted of seven questions in three sections. The first section addressed the existing fixing process and asked three questions under the title 'Feedback on use of Current Price". The remaining two sections solicited the participants' opinions about the future of the silver fixing process. One of these sections with two questions was titled "Possible improvements to London Silver Price mechanism", while the other section, also with two questions, was headed "Silver Price Contributors". On 23rd May, a week before the survey closing date, the LBMA published a press release providing an update on the online survey, saying that the survey had at that time received over 250 responses and that market respondents indicated "the need for transparency and wider participation in any future price discovery mechanism". On 5th June, the LBMA announced the final results of the survey, stating that based on over 440 survey responses: "the general consensus was that the silver pricing mechanism should be an electronic, auction - based solution. The solution must be tradeable, with an increased number of direct participants. More specifically, the responses to each of the questions are summarised below:" However, the LBMA press release then only proceeded to summarise the responses to four of the seven survey questions, these being the simple yes/no, multiple choice, and 1-10 ranking questions. There was no reference in the press release to the fact that there had been three additional questions in the survey about the future of the silver fixing, and misleadingly, the LBMA listed their summarised questions/answers as Q1, Q2, Q3, and Q4, as if there had only ever been four questions in the survey. More importantly, of the four questions that the LBMA's answer summary did mention, three of these were related to the existing process "Feedback on use of current price", and only one related to the future process, a quite innocuous question, namely "Would you consider acting as a contributor?" The three questions that were arguably the most critical questions in the survey were simply not addressed or even mentioned by the LBMA. These three questions were:

Not only was there no mention of the fact that these three questions even existed in the survey, but having the responses of over 440 survey respondents to three critical questions on the future of the silver pricing mechanism simply reduced to a few buzz words of a "general consensus" for an "electronic, auction - based solution" "tradable" with an "increased number of direct participants" is, in our view, not very transparent. In fact, it's quite misleading. What happened to the non-consensus views amongst the respondents? It's interesting that the LBMA phrased the question on ideal contributors as a leading question, prompting with some examples and listing 'bullion banks' first. This is quite ironic given that bullion banks are the very entities who perpetuated the downfall of the existing silver fixing process, and who have in other fixings, such as the gold fixing, been seen to be far from 'ideal contributors'. Without acknowledging any dissenting views on 5th June, the LBMA then proceeded full steam ahead, on the same day, to launch a 'Request for Proposals' (RfP) for companies that might be interested in 'administering' this new electronic, auction based, silver price discovery process. On 19th June, the LBMA announced that the seminar, to take place the next day on 20th June, would be open to LBMA members, ISDA members, and other bullion market participants, and that the Bank of England and Financial Conduct Authority (FCA) would attend the seminar as 'observers'. Crucially, the LBMA statement said that the seminar would take place under the Chatham House Rule. According to Wikipedia, the Chatham House Rule "is a system for holding debates and discussion panels on controversial issues."

Hardly the makings of transparency. By holding the silver price seminar under the Chatham House Rule, how does this support the "need for transparency" that market participants in the survey indicated that they desperately desired? And why the Bank of England needs to be at a silver price seminar when they hold little or no custody of silver is anybody's guess. Perhaps the Bank of England still views silver as a monetary metal and as an important strategic asset? Furthermore, on what basis did the LBMA think that the seminar might get into the discussion of controversial issues that would require the use of the Chatham House Rule? After all, they had stated only two week previously that there was a 'consensus view' on an 'electronic, auction based system'. In their statement on 19th June, the LBMA revealed that the seminar would host presentations by potential solution providers for the London Silver Price mechanism. Participants would be given a follow up survey in which to give their feedback, but, according to the press releases, only LBMA members would "be asked to confirm which solution they will be willing to participate in with effect from 15th August". It was on this day also that it was also revealed that there had been submissions to the LBMA from ten solutions providers that were interested in administering the silver price process, but that only seven of these ten had made the short list, and that only these seven would be presenting at the seminar. The short list consisted of the London Metal Exchange (LME), CME Group / Thomson Reuters, Intercontinental Exchange (ICE), ETF Securities, Bloomberg, Autilla Ltd (Cinnober Financial Technology of Sweden) and Platts. The solutions of these seven applicants were said to have met the criteria of the LBMA's Request for Proposal, which were revealed to be that a solution provider Proposal be electronic, auction-based and, 'auditable'. On 19th June, the LBMA also announced that "Executive summaries of the proposed solutions will be circulated to the press by the LBMA early next week". More interestingly, they said that: "Copies of (the next day's) presentations will be posted on the Members' Section of the LBMA website". Again, this does not sound very transparent, that all seven presentations of the seven solutions providers would only be made available to LBMA members and not to the wider market. On Friday 11th July, the LBMA announced that CME Group and Thomson Reuters had been selected to 'provide the solution' for the London Silver Price mechanism "following the market consensus that has recently emerged". It appears that by 11th July, a 'general consensus' had suddenly turned into a 'market consensus' since, after "numerous meetings with market participants, solution providers and regulators", "the second survey indicated a clear market consensus for the CME Group & Thomson Reuters proposal". The LBMA said that the CME/Reuters proposal met the Proposal criteria "as it is electronic, auction-based and auditable. It is also tradeable with an increased number of direct participants." But surely all seven shortlisted proposals met the Proposal criteria? In fact, all seven proposals did meet the criteria; that was why they were on the short list in the first place (see 19th June LBMA statement about the short list). Stating that there was a "clear market consensus" for CME/Reuters without backing it up, is about as transparent as saying that there was initially a "general consensus" for an electronic auction platform; i.e. neither statement is transparent without publically available supporting evidence, of which there was none. The LBMA statement on 11th July also said that the market consensus was supported by an "independent review" of the seven short listed companies by Jonathan Spall of G Cubed Metals Ltd.

The LBMA stated that feedback from the surveys, the submissions and "the conclusions of the independent review" "were presented directly to a meeting of the LBMA Management Committee, LBMA Market Makers and the Data Working Group." Again, where is the transparency in this, and why was the wider market not privy to these presentations to the LBMA? On 24th June, the LBMA published some presentation material from the proposals of the seven shortlisted solutions providers who had presented at the seminar on 20th June. Specifically, the LBMA stated "Seven proposals were presented at the seminar, executive summaries and/or slides (as appropriate) are set out below:" However, when you view the selection of material that the LBMA published on its site for each of the seven applicants, it quickly becomes apparent that the material released by each applicant is not standardised or consistent. Autilla allowed the LBMA to publish their slides and their executive summary. Platts allowed the publication of their slides. ETF allowed the publication of their slides and their original RfP response. However, Bloomberg, the LME, ICE and CME/Reuters only allowed publication of their executive summaries. Recall from 19th June that the LBMA had said that "Executive summaries of the proposed solutions will be circulated to the press by the LBMA early next week", but that "Copies of presentations will be posted on the Members' Section of the LBMA website" (see reference below). For the winning entry, CME/Reuters, the LBMA reasoned that the CME/Reuters, by not publishing their slides, were protecting the specification and software of their offering. Given that the presentations all appear to have been "posted on the members' Section of the LBMA website', this again begs the question, where is the transparency in this new silver price setting process? The entire process has been a bit of a shambles. The Gold Anti Trust Action Committee (GATA) and those concerned about price manipulation will allege that the LBMA and the western bullion banks are engaged in a rebranding and repackaging exercise in order to maintain a cosy gold and silver cartel of bullion banks and ultimately control over precious metal prices.

It is difficult for the LBMA to claim that the new silver pricing process is transparent. Thomson Reuters need to be careful that they are not being used to rubber stamp the new LBMA silver pricing mechanism. Regulators need to look at the process and institute a new pricing mechanism and ensure that the price of silver is based on real physical precious metals supply and demand between government mints, refiners, miners, manufacturers, jewellers and of course investors. London Silver Market Fixing Company Ltd announces end of silver fixing, 14th May http://www.reuters.com/article/2014/05/14/idUSnMKWWsY3ca+1e8+MKW20140514 LBMA announcement on The London Silver Market, 14th May http://www.lbma.org.uk/_blog/lbma_media_centre/post/the-london-silver-market/ LBMA announces London Silver Price - market consultation, 16th May http://www.lbma.org.uk/_blog/lbma_media_centre/post/MARKETCONSULTATION/ LBMA announces London Silver Price – consultation update, 23rd May http://www.lbma.org.uk/_blog/lbma_media_centre/post/consultationupdate/ LBMA announces London Silver Price consultation survey results, 5th June http://www.lbma.org.uk/_blog/lbma_media_centre/post/SILVER_SURVEY_RESULTS/ LBMA announcement about the 20th June silver price seminar, 19th June http://www.lbma.org.uk/_blog/lbma_media_centre/post/seminarupdate/ LBMA silver price solution - CME Group and Thomson Reuters http://www.lbma.org.uk/_blog/lbma_media_centre/post/silverpricesolution/ LBMA 2014 Silver Price Consultation Seminar GoldCore discussed the risk of the new silver and gold fixes remaining non transparent in a recent interview - see here (3 votes) |

[This story was updated Aug. 15, 2014] The much-maligned London

[This story was updated Aug. 15, 2014] The much-maligned London

I shall come to this important event later in this market report; but first, our customary look at this week's trading. From Monday through Wednesday the gold price found firm support at the $1305 level before gaining a few bucks to $1313 by close of play last night.

I shall come to this important event later in this market report; but first, our customary look at this week's trading. From Monday through Wednesday the gold price found firm support at the $1305 level before gaining a few bucks to $1313 by close of play last night.

| You are subscribed to email updates from Silver prices - Google Blog Search To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 Comment for "Silver prices | Here's What the New Silver Price Fix Means for Prices"