Is Oil About To Follow <b>Gold</b> Down? This <b>Chart</b> Says It Will. [EOG <b>...</b> |

- Is Oil About To Follow <b>Gold</b> Down? This <b>Chart</b> Says It Will. [EOG <b>...</b>

- Calafia Beach Pundit: 10 <b>charts</b> to watch

- Barrick <b>Gold</b>: Have We Seen The Bottom? - Seeking Alpha

- Gold Correction Isn't Over, But <b>Gold Price</b> Heading to $20,000 :: The <b>...</b>

| Is Oil About To Follow <b>Gold</b> Down? This <b>Chart</b> Says It Will. [EOG <b>...</b> Posted: 06 Dec 2013 03:47 PM PST Anybody who follows financial markets knows the direction of gold prices over the past year. This is not a secret. But what seems to be lost or hidden somewhere in the deep recesses of investors short memories is where EVERYONE "knew" that gold was going just one short year ago. Yes, most people have long forgotten their fail-safe plans to strike it big with their gold stocks and gold ETFs such as GLD. (If you got in at the right time, you DID make a killing on gold) And why shouldn't they, after all, the stock indices are reaching for all-time highs on a daily basis. Who needs gold when we have the stock market? It seems that CNBC has a different financial pundit on every hour that shouts from rooftop, "THIS IS NOT A BUBBLE." But I caution everyone, if we learn nothing from the past, then we deserve to lose. And just like with gold, most of us will, unless we heed the warning signs. Cyril Kornbluth may have been right, when he coined the phrase, "the only thing we learn from history is that we never learn anything from history." Gold Prices from October 2007 to October 2013 - Weekly Chart With that said, I want to turn our attention to the gold chart above spanning from October 2007 to October 2013. Notice the chart pattern formed here and highlighted by the red lines is a bullish pennant pattern. A bullish pennant pattern is a pattern that pauses to consolidate into a pennant shape and then continue higher. You can see from the chart, that there are 2 points labeled where the pennant tried to break above resistance and failed before completing the pennant pattern. Then it tried to break out a 3rd time only to fail once more. Please make a mental picture of this pattern. Gold Prices from October 2007 to October 2013 - Weekly Chart Taking a look at this chart, you can see that around the time QE3 was announced was when it made its 3rd and final attempt to break above resistance. EVERYONE was saying buy gold. Instead, gold did a nose-dive, and broke through several resistance levels to decline over 35% and will likely decline even further yet. And what are financial headlines saying about gold now?

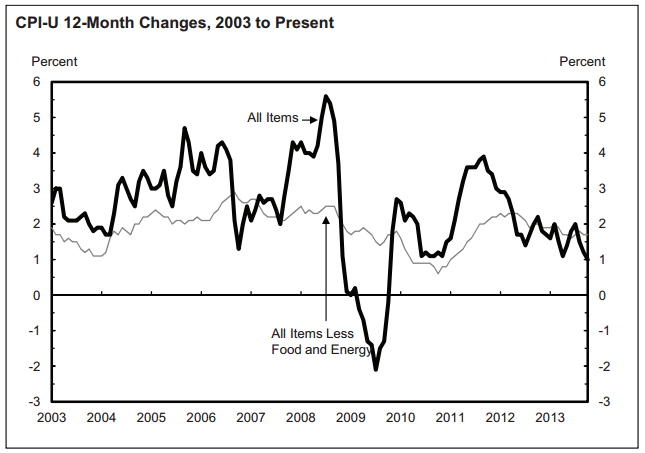

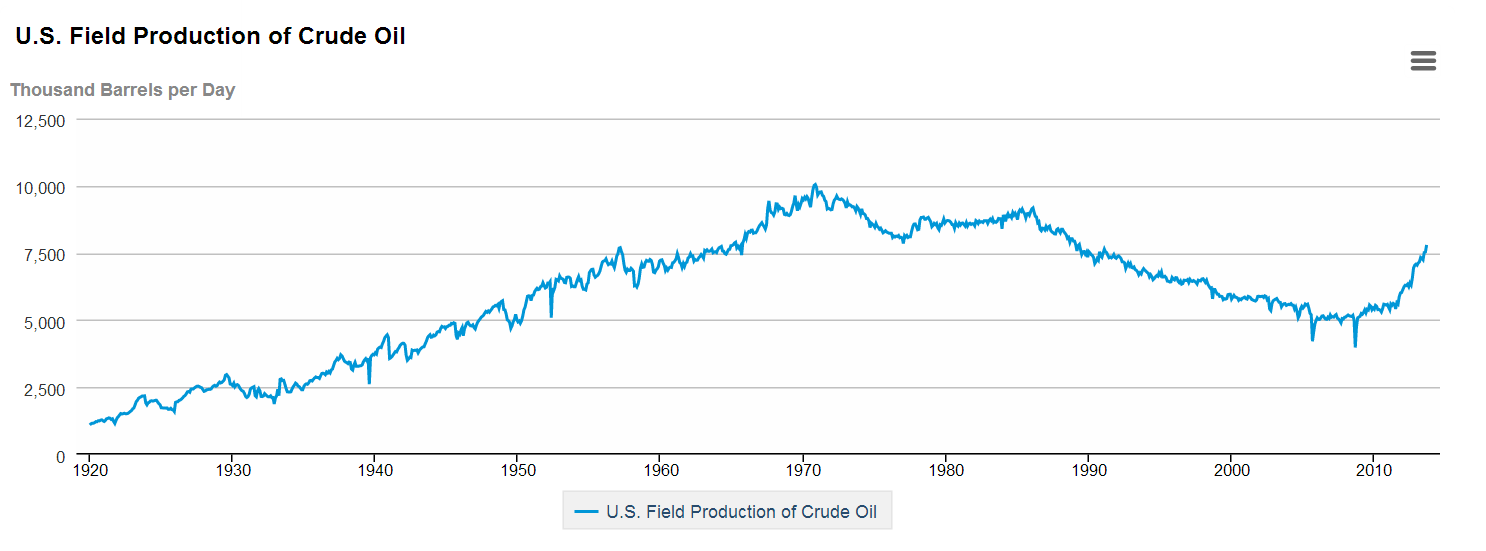

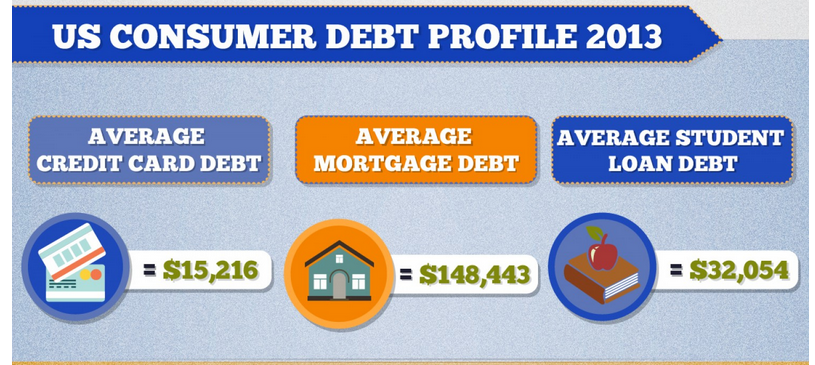

Notice how the headlines say that gold is falling because of tapering fears, or a strong economy in general. And yet, gold prices are far lower than when QE3 even began. Don't listen to the headlines, they are only there to sell advertising. Its very simple why gold is going down. Gold reached a point where the buyers of gold were exhausted and there were fewer people left to purchase gold, versus sell gold. Why are buyers exhausted? For nearly a decade, people have been buying gold furiously due to expected inflation, record government debts, and a number of sovereigns buying large amounts of gold. As a side note, sovereigns are always reactionary, and will be the last one to the party, so if they are doing one thing, then it is wise to do the opposite. But back to the fact that sellers over powered the buyers. We can argue about the reasons behind this phenomenon for hours and still not fully understand it. But the real reason we are here, is because what happened to gold, is the same thing that is about to happen to crude oil. Oil Prices from October 2004 to October 2013 - Weekly Chart Look at the oil chart above during the same time period. The first thing one should notice is that the oil chart looks very similar to the gold chart. Second, it is a much more dramatic from the standpoint of time and price movement. The Oil chart ranges in price from $147 to $35 and everywhere in between. Just like gold, there are the first 2 points labeled where it tried to break out and failed. It then continued to form the pennant pattern before trying to break out a 3rd time on the news related to Syria this past summer. Only, just like gold, it has failed and is beginning its decline. How far will it decline? Who knows, but given the length and size of the pennant formation in this chart, it will probably move slower and possibly further on a percentage basis than gold. What have the financial pundits been saying about oil? They are saying "buy" because the fed is trying to cause inflation, the Mideast is unstable, and sovereigns have record levels of debt. The scary thing is, they are saying buy oil for the same reasons they told everyone to buy gold. Just like gold, the financial pundits are about to be proven wrong again. Even with the Fed's best efforts to cause inflation, the October CPI just decreased by .1% and you can see from the CPI chart below that despite the Fed pumping $85 billion into the system each month, inflation is trending downwards. Supply and demand is a much more reliable metric to tell us where oil prices might be going. Look at the oil chart below and see the US production. When you couple that with the weak demand caused by an over leveraged, troubled economy, the supply and demand picture for oil is weak. It would be wise to stay away from oil investments such as this oil ETF, USO. Source: BLS Source: EIA So what does the oil market outlook tell us about the greater economy? Be careful to not listen to financial pundits when oil prices begin to plummet. What they will say is to "buy the stock market" because low oil prices are good for the overall economy. Common sense would tell anyone this is true and it doesn't take an MBA to figure this out, but lets try to think a little deeper than that before we believe the financial talking heads. We should look back over the past few years and see what was happening in the economy when oil plummeted from $147 to $35 in 2008, or when oil went from $115 to $75 in a couple months in 2011. Second, lets ask ourselves why does the Fed need to target annual inflation rates of around 2 percent? Why don't they just try to keep inflation at 0? Put another way, why is a rising price environment so important to the Fed? Quite simply, the Fed's job is to make BAD DEBT TURN INTO GOOD DEBT. The economy that we now live in, is overleveraged with everything from credit card debt, to mortgage debt to, to student debt. (not to mention government debt) And if we were to fall into a deep deflationary cycle, it would spell disaster for our economy. Source: Visual.ly Look at the graphic above for the facts in 2013 related to consumer debt. When a society becomes so leveraged to the point US citizens are, there is less money to spend and when there is less money to spend, things begin to deflate. When things begin to deflate, "bad debt" becomes "worse debt" because things are worth less. So although lower oil prices are good for the economy, and ultimately you and I(the consumer), it is going to be a sign of the deflationary cycle that is already in motion. If that is coupled with a rising interest rate environment, you have the makings of a perfect storm. But interest rates are a conversation for another day. Two previous articles that I wrote talked about going long on two of what I believed to be the best oil & gas companies in the stock market. Those being Magnum Hunter Resources (MHR) and EOG Resources (EOG). These two stocks have treated investors well over the past 6 months, but with where I've just outlined prices going, these stocks should be avoided. I still love almost everything about these two oil companies. I just no longer like crude oil which is a large part of these company's portfolio. Hopefully this was helpful to give you a different perspective on oil prices and the economy at large. The truth is in the charts and one cannot deny that despite the Fed's best efforts, we are entering a deflationary period. Remember, Soren Kierkegaard was right when he said, 'Life can only be understood backwards; but it must be lived forwards.' Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. |

| Calafia Beach Pundit: 10 <b>charts</b> to watch Posted: 10 Dec 2013 01:13 PM PST In my view, market-based data are better indicators of what is going on beneath the economy's surface than official statistics. Market-based data are usually available in real-time, and they are derived from the interactions of millions of participants from all over the world—the wisdom of crowds distilled into one number. They aren't seasonally adjusted, and they aren't subject to revisions after the fact. But they do require some interpretation, so here is a collection of 10 market-based indicators that I'm paying attention to, and why. On balance, I think they all reveal a gradual improvement in the economic and financial fundamentals, but the persistence of a general aversion to risk.  Gold and commodity prices tend to track each other over time, but gold is much more volatile (note that the range of the y-axis on the right is about twice the range of the same y-axis on the left). Gold tends to lead other commodity prices, being the most speculative of them all. Gold also is unique among commodities since all the gold ever mined throughout history is still held by someone somewhere, whereas most other commodities are either incorporated into other stuff, consumed, or deteriorate with time. Gold is the classic refuge from inflation, geopolitical risk, and just plain uncertainty. It's a darling of speculators, perhaps because it's price can go up or down enormously and it's widely held. What the chart above tells me is that gold overshot the prices of commodities in the early years of the current recovery—in part due to concerns that the Fed's QE program would lead to hyperinflation—and is now in the process of realigning since inflation remains low and stable. Industrial commodities have been relatively stable for several years now, and gold looks to be in the process of coming back down to a level that is more consistent with the current level of industrial commodity prices. I note that over the past century, the real price of gold in today's dollars has averaged just under $600/oz.   The two charts above zoom in on the prices of gold and industrial commodities over the past 5 years. Gold looks like it's having a tough time maintaining its current lofty levels, while industrial commodity prices have been unusually stable for the past two years.  Gold prices have tracked the inverse of the real yield on 5-yr TIPS amazingly well over the past seven years. (Think of the inverse of real yields as the price of TIPS.) The world was willing to pay ever-higher prices for gold and TIPS through 2012 because—as I see it—the world was desperate for safe assets that also offered protection against inflation. Prices for both were bid up to extremely high levels (corresponding to strongly negative real yields on TIPS) which reflected deep-seated pessimism and very bearish expectations for the future. Instead of doom and gloom, we have since seen inflation remaining low and economic growth fundamentals in the U.S. improve on the margin. Both TIPS and gold are thus facing selling pressure. Still, at current levels both reflect a fairly strong demand for risk-free assets, and thus reflect a market that is still moderately risk-averse.   The two charts above track nominal and real yields on Treasuries, and the difference between the two which is the market's expected inflation rate. If anything stands out, it is that expected inflation hasn't changed much in the past 16 years. The market currently expects inflation over the next 5 and 10 years to average a little over 2%, and that is very close to what inflation has actually averaged over the past 5 and 10 years. This tells us that the market does not see believe that the Fed's QE policy will be inflationary. Should that change, and if expected inflation were to begin rising, that would be very significant, since it would presage a significant increase in interest rates and a more rapid than expected shift by the Fed to tighter monetary policy.  Real yields on TIPS should tend to track real growth expectations for the U.S. economy. Very strong real growth inevitably leads to strong real investment returns, and TIPS need to compete with that by offering higher real yields. For the most part this has been the case, as the chart above shows. Currently, however, there is a rather large gap between the two, which to me suggests that the market worries that U.S. growth will slip below 2% in the next few years. I take this to mean that the market is pessimistic and risk-averse. But if real yields continue to rise, that would be a clear sign of a return of optimism and/or a decline of pessimism. The higher real yields on TIPS go, the more optimistic the market is about the prospects for U.S. growth.  The Baltic Dry Index measures the cost of shipping bulk commodities in the Asia/Pacific region. It is a function of two major variables: the supply of shipping capacity and the demand for shipping capacity. Prices were depressed for most of the past several years because of a significant increase in shipping capacity. More recently they have rebounded rather strongly, presumably because economic activity is continuing to increase (e.g., Chinese demand for coal from Australia) while shipping capacity is relatively constrained. As such, this appears to be signaling a somewhat stronger global economy, which would in turn support a stronger U.S. and Eurozone outlook.  The chart above shows that there has been a very strong inverse correlation between the value of the yen and the Japanese stock market. The yen was extremely strong from 2007 through 2011, and the Japanese stock market lost over half its value. That tells me that the yen was so strong (and by inference, Japanese monetary policy was so tight) that it damaged the outlook for real growth by creating deep-seated deflationary expectations and disrupting Japan's ability to compete. Consumers could make money just by holding on to their cash, for example, rather than spending it. Japanese manufacturers faced extreme difficulties competing with overseas rivals due to the incredibly strong yen, which made Japanese goods uncompetitive. The outlook for Japan has brightened considerably in the past year, however, since the Bank of Japan adopted an aggressive policy easing stance. This has allowed the yen to return to non-deflationary levels, and that in turn has allowed Japanese manufacturers to more effectively compete in the global marketplace, and convinced consumers to save less aggressively. If the yen were to strengthen again, that would be a bad sign for the stock market and the global growth outlook.  Swap spreads have been very good leading and coincident indicators of the health of financial markets and the economy. U.S. swap spreads have been exceptionally low for the past year or so, a reflection of abundant liquidity and extremely low systemic risks. Eurozone swap spreads have been substantially higher, in contrast, reflecting ongoing problems with sovereign default risk. However, the recent decline in Eurozone swap spreads stands out: this is the lowest they've been since pre-recession days. Fundamentals in the Eurozone are likely improving significantly on the margin, and that is good news for just about everyone.  Corporate credit spreads continue to decline, and that suggests that the outlook for the U.S. economy continues to improve. Spreads are still somewhat high relative to pre-recession periods, however, suggesting that the market is still somewhat cautious. The persistence of risk aversion in U.S. markets suggests that risk assets are not yet in a bubble.  The PE ratio of the S&P 500 is only slightly higher than its long-term average, despite the fact that corporate profits are at all-time highs, both nominally and relative to GDP. This is another indicator that risk aversion persists and that equity valuations are still somewhat attractive.  As the chart above shows, Eurozone equities have significantly underperformed their U.S. counterparts in the past few years. The Eurozone economy has been in a recession for most of that period, so this is understandable. The Eurozone economies are now emerging from recession but are still plagued with sluggish growth. Nevertheless, the 12-month trailing PE ratio of the Euro Stoxx index is about the same as the PE ratio of the S&P 500 (both are just under 17), but the forward PE ratio of the Euro Stoxx index is 13, as compared to 15.4 for the S&P 500. This suggests that caution and risk aversion are somewhat more pronounced in the Eurozone, which makes sense given the problems that persist in many of the weaker Eurozone economies. On balance, I don't see that Eurozone stocks are more attractive than U.S. stocks, but there could come a time when the relative valuations of U.S. and Eurozone stocks reveal an attractive investment opportunity. |

| Barrick <b>Gold</b>: Have We Seen The Bottom? - Seeking Alpha Posted: 10 Dec 2013 12:57 AM PST As a contrarian investor I am looking for bargain companies with outsized return potential and a high margin of safety. What potential is and how it is measured is often basis for discussion. Many investors will see zero potential in Barrick Gold (ABX) or MGIC (MTG) or J.C. Penney (JCP) simply because they are influenced by disruptive short-term events and negative headlines. Negative events often overshadow the true intrinsic long-term value of a company as many investors believe they are superior market timers. I think that investors who purchase stocks at discounted prices when nobody else wants them and they intend to hold their investments for the long-term, they will indeed do well in the long-term. A long-term investment approach fundamentally changes the mindset out of which an investor approaches investments and short-term distractions, noise and negativity just fall aside. Barrick Gold is such a contrarian investment. The company has fallen on hard times as the gold price declined substantially over the last two years and shares of Barrick Gold as well as other gold- and copper miners fell off a cliff: (click to enlarge) The share price of Barrick Gold has fallen more than the underlying gold price as investors feared a continued decrease in gold prices. As such, gold bears display a textbook example of representativeness bias in which investors simply extrapolate current events in the marketplace that is, persistently low and/or falling gold prices). As negativity increases so does the differential between share price and intrinsic value. It is clearly not easy to stay focused and positive when confronted with a wave of bad news. The chart below depicts the gold spot price over the most recent two years and shows why gold investments turned out bad. (click to enlarge) In light of crumbling gold prices, Barrick Gold does the right things for shareholders. The company just recently announced a $3 billion equity offering in order to gain financial flexibility and decrease financial leverage. In addition, Barrick Gold is focused on bringing capital expenditures down via a suspension of its Pascua-Lama mine operations in Argentina/Chile (this should relieve cash flow by about $1 billion in 2014). Further, the company streamlines its portfolio and booked $700 million in non-core asset sales YTD in 2013. Barrick also has a comprehensive cost reduction program in place that aims at cutting off $500 million of the cost structure. Going forward, I could see a sale of copper operations or a mine-/cost-sharing project with a strategic partneras further catalysts. Long-term fundamentals still intact Gold is a precious commodity that not only finds applications in the jewelry and electronics sectors of civilization. Investment demand for gold bars and coins also contributes to the desirability of this commodity and its reputation as a safe heaven investment was proven during the financial crisis as the gold price spiked amid extreme levels of economic uncertainty. Jewelry, of course, is the most relevant sector in the consumption sphere and demand from China and India could be instrumental in driving gold prices over the next decade or two. Growing and richer Asian economies will exhibit higher jewelry demand as Asian societies view gold jewelry as a sign of social- and economic mobility and success. Jewelry- and industrial demand are going to increase in the long-term as Asia lifts hundreds of millions of people out of poverty. Gold also has high conductivity and therefore finds irreplaceable applications in electrical wiring and contacts. Investment demand will exist as long as people invest in stocks and bonds and need a safe heaven when other non-commodity asset classes undergo stress. Furthermore, gold investments provide investors with substantial diversification benefits especially when hold in equity- and bond dominated portfolios. Market valuation The reasons why I am particularly attracted to Barrick Gold are threefold. First, I believe the company takes the right steps for shareholders in reducing costs, realigning capex with profitability, selling non-core assets and improving the balance sheet. Secondly, Barrick Gold is a large-scale gold explorer with significant tech know-how and experience which helps in providing the company with a cost advantage. Barrick's estimated 2013 all-in sustaining costs are projected to hit $900-975/oz which compares to $1,150-1,225/oz for other senior gold producers. Thirdly, Barrick Gold shares have been driven down to such low levels that the company is just dirt cheap. Barrick Gold trades at less than eight times forward earnings while the peer group average stands at 14.52. Goldcorp (GG) and Kinross Gold (KGC) trade at the highest P/E multiples of 19.88 and 18.32 respectively. The median of the peer group comes out at 15.53 which still is about twice as much as the P/E ratio exhibited by Barrick Gold. (click to enlarge) Conclusion Long-term gold price drivers are fundamentally intact. Investment-, jewelry- and industrial demand are secular trends that will affect the gold price in the long-term. At the same time, new gold discoveries are rare which adds to the favorable long-term supply/demand picture of the gold commodity. In addition, gold provides investors with significant diversification benefits which can help reduce overall portfolio volatility. Most importantly, Barrick Gold trades at a ridiculous valuation. A multiple of eight times forward earnings translates into an earnings yield of 12.6% which is inappropriate for an industry-leading, large-cap heavyweight in the gold sector. Other companies in the gold sector command significantly higher multiples; most noteworthy is Goldcorp with a multiple of almost twenty. Barrick Gold also moves aggressively to counter weak gold prices through non-core asset sales and cost reductions. Strong anti-cyclical BUY on valuation, favorable long-term gold price drivers, cost cutting initiatives and portfolio diversification benefits. |

| Gold Correction Isn't Over, But <b>Gold Price</b> Heading to $20,000 :: The <b>...</b> Posted: 10 Dec 2013 12:39 PM PST By: Casey_Research

|

By Louis James, Chief Metals & Mining Investment Strategist

By Louis James, Chief Metals & Mining Investment Strategist

| You are subscribed to email updates from gold price graph - Google Blog Search To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 Comment for "Is Oil About To Follow Gold Down? This Chart Says It Will. [EOG ..."